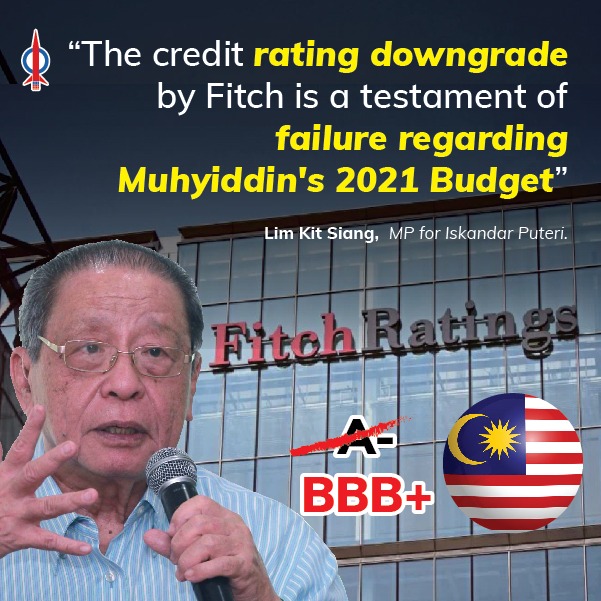

Fitch’s downgrade of Malaysia’s long-term foreign-currency issuer default rating (IDR) from A- to BBB+ is an indictment of the 2021 Budget presented by the Finance Minister, Tengku Zafrul Abdul Aziz to Parliament early November.

I have read the Fitch Report and the statement from the Minister of Finance.

It is somewhat pathetic as rebuttals go. The case made out lacks credibility as it is largely built on repeating the usual ” feel good ” numbers and assertions.

It fails to address many of the issues that the Fitch Report raised e.g. weak governance, poor record on corruption, low revenue, enhanced debt and loan guarantees etc., None of these concerns have been addressed by the Minister.

We should not be slavish to the perspectives of rating agencies, as Malaysia and the world are facing “once-in-a-century” Covid-19 pandemic, which has grown increasingly worse despite a year of rampage, claiming nearly 67 million infections and over 1.5 million deaths.

Three days ago, the world registered a record-high daily increase of 688,333 cases, with the United States reaching a record-high daily increase of 237,328 cases yesterday.

Although the Covid-19 vaccine is poised to be approved and distributed in the coming weeks, it is not going to alleviate the record levels of infections and hospitalizations in the United States, which has suffered nearly 15 million Covid-19 infections and over 287,000 Covid-19 fatalities.

The world has almost reached the 67 million mark for cumulative total of Covid-19 cases and is heading towards the 100 million mark, which will probably be reached in Joe Biden’s 100 days as the 46th US President.

We should have an extraordinary budget in extraordinary times, but unfortunately Tengku Zafrul’s budget is a very ordinary budget in extraordinary times.

While we must be prepared to do extraordinary things in extraordinary times to help vulnerable groups, as well-known Malaysian economist K.S. Jomo has rightly reminded the government, it is no excuse for corruption or abuses of power.

Valid and credible criticisms in the Fitch Report should be addressed.

The Fitch Report uses data from reliable sources including the World Bank and the reasons for the downgrade will be harder to counter as the necessary reforms will be difficult given the shaky government which is rudderless.

It lacks the strength to launch long overdue reforms e.g. fiscal consolidation, greater transparency and accountability. The policy stance thus far, as elaborated in the Budget, has been far from robust.

The Fitch Report has to be read with care. Between the lines one can discern a sharp message that questions the Budget strategy e.g. the issue of “stimulus“ without reforms or spending your way out of trouble. The handouts to the suffering masses are not sustainable as the fiscal position does not permit.

Other rating agencies are likely to follow suit in downgrading Malaysia’s credit worthiness.

The direct implications linked with the downgrade are a) it will affect the cost of borrowing by the government of Malaysia; b) potential investors, both foreign and domestic, will think twice about investing in Malaysia.

In brief, we are heading for a bleak outlook with powerful market forces unleashed.

It is noteworthy that there do not appear to be downgrades thus far for other ASEAN countries.

It further weakens Malaysia’s competitiveness. It also has implications in terms of our foreign relations e.g. we are likely to become more dependent on China for loans to fund large scale projects which are favoured by the Government.

We may also see an impact on the exchange rate e.g. the Ringgit taking a hit. There may also be an acceleration in capital flight.

Painful reforms are clearly needed but will they be forthcoming in a kakistocracy?

The revenue side of the Budget will require close and urgent attention. There will be a need to trim expenditures –for instance, we do not need a Cabinet of 30 odd Ministers or RM81.5 million allocation for outfits such as JAKIM.

The government will have to bite the bullet either voluntarily or will be forced into doing so by the IMF much in the way Indonesia was forced in 1998.

There is an urgent need to conduct a comprehensive Public Expenditure Review to shape a strengthened fiscal system. This needs to be accompanied by deregulation of rules and processes so as to create an environment which deters corruption.

While it is true that COVID-19 has hurt the economy, the reality is that for 20 odd years we have run deficits and kept going on borrowings.

We have continued to tighten the regulatory regime and failed to promote competition. We have acted as if there is no tomorrow – acting like an addict.

It is thus all the more urgent that fiscal reforms together with other economic reforms get launched. Bipartisan agreement on the issue of reforms are needed to pull the country from the edge of a dangerous cliff.

But there is no running away from the fact that the Fitch downgrade is an indictment on Muhyiddin’s 2021 Budget.

Lim Kit Siang

MP for Iskandar Puteri